2026 Shareholder Advocacy and Engagement Report

Our Engagement in the Age of DEI-Hushing and Changes to Shareholder Resolution Processes

By Elizabeth R. Levy, CFA, shown above speaking on a panel at the US SIF conference in June 2026

Shareholder advocacy and engagement have their own calendar, which works backwards from the Annual General Meeting (AGM) season’s peak in May and June. As we at Clean Yield plan for what to expect in next year’s season, we reflect on the prior year’s work, July 2025 through June 2026.

Shareholder advocacy and proxy voting are critical tools equity investors use to influence corporate decision-making and drive systems-level change. For more details and background on how shareholder advocacy works, review our two reports, each of which includes a breakdown of how engagement and proxy voting work.

In the report below, you’ll find:

- A summary of the current environment

- A review of our 2025-26 dialogues and engagement

- A synopsis of our proxy voting activity

Stay up to date with the impact investing landscape with our newsletter.

Clean Yield uses the power of investment and markets to help our clients achieve their financial goals and move society toward a more just and sustainable future. Discover more about our work, the change we seek, and our efforts to make a positive impact.

The Current Environment

DEI’s Cold War

For the second year in a row, it would be impossible to talk about our engagement activities this year without acknowledging the changing climate in which they occurred. Last year, we noted the ongoing war on anything considered “woke,” most notably on anything pertaining to Diversity, Equity, and Inclusion (DEI). This year, the war turned into more of a cold one, with companies voluntarily dropping public mentions of anything DEI-related, presumably to avoid the ire of the anti-DEI regulators.

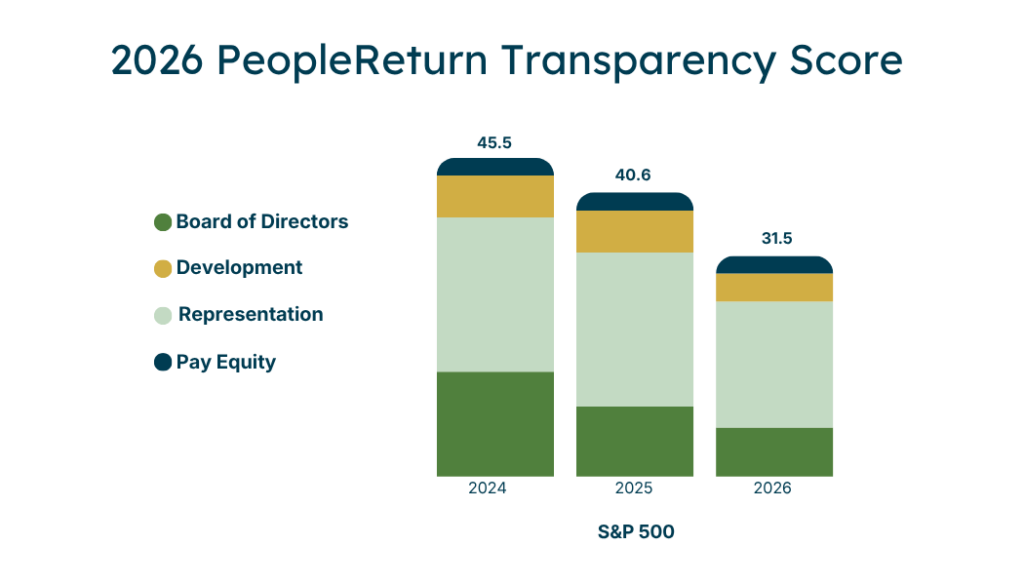

According to data from PeopleReturn, which itself used to be called DiversIQ, for S&P 500 companies, “leadership-level gender disclosure fell from 86.0% in 2024 to 62.2% this year. Race/ethnicity disclosure fell from 72.5% to 47.6%. More granular racial and ethnic group disclosure fell from 47.6% to 31.4%.” These disclosures are set to fall even further, as the Equal Employment Opportunity Commission proposed in May to stop mandatory collection of the EEO-1 data set of metrics on employee workforce demographic data by job category, sex, and race or ethnicity, which underpins this disclosure.

Chart data from PeopleReturn.

At the same time, diversity on corporate boards is falling. A March 2026 “Board Monitor 2026” report found that within Fortune 500 companies, “After years of progress, 2025 saw the lowest share of seats filled by both women [31%] and non-white [29%] directors since at least 2016.”

Despite this apparent retreat, shareholder responses to so-called “anti-DEI” proposals are not any warmer than they were last year. Looking at data through May, the Harvard Law School Forum on Corporate Governance reports that the 22 anti-DEI proposals voted on by that point attracted on average 1% approval, well below the 13% average approval that the five “pro-DEI” proposals garnered. The analysis also called out the dramatic decline in the number of pro-DEI proposals overall, suggesting that the legal climate has made companies fearful to talk about DEI information and shareholders fearful of asking for it.

Process Changes

“DEI-hushing” was not the only change to the shareholder advocacy climate this year. Last year, we noted that the Securities and Exchange Commission (SEC), the government agency that has a mission to protect investors, under the new Trump administration, began making changes to the shareholder resolution process immediately, and those changes continued into this year. As we described earlier this year, the SEC announced in November 2025 that companies could omit proposals received from shareholders from their proxy statements by notifying the SEC, rather than by obtaining the SEC’s permission as they had under prior rules. The SEC also limited the way that shareholders share and communicate information on the proposals filed.

The result of these changes, according to an April analysis by the Shareholder Rights Group, which Clean Yield is a member of, resulted in approximately 20% fewer proposals being filed for the 2026 season. However, companies availed themselves of the exclusion process less than in prior years; as the report suggests, “unilateral exclusion carried too much risk, including proponent litigation, reputational risk, potential fuel for a proxy fight over director elections, and other concerns.”

In the fall and again in early summer, we attended a “Hill Day” (pictured above), visiting Congressional offices with other like-minded investors to raise awareness of the issue of shareholder voices being silenced. One of our takeaways from these visits is that corporate lobbyists are getting their message heard clearly, and we need to keep making sure folks on Capitol Hill hear from sustainable investors as well, which is why we keep attending.

Despite the changes made to the shareholder resolution and proxy voting processes already, there is fear in the shareholder advocacy community that even more draconian changes may be coming, up to and possibly including restricting the ability of investors such as Clean Yield to file resolutions at all. We find that our participation in groups like the Shareholder Rights Group (SRG) allows us to continue to advocate for our rights as shareholders. This spring, we interviewed SRG’s Sanford Lewis about the changes to the process and encouraged our clients and community to sign a petition that encourages the SEC to maintain these shareholder rights, which is available at the Defend Shareholder Rights site. In addition, we hosted a panel discussion (see the featured image at the top of this post) at a conference hosted by the US SIF (the Forum for Sustainable and Responsible Investment) in June on how to keep engaging with companies if the shareholder proposal process is no longer available. Should that come to pass, we expect our Shareholder Advocacy program to change but remain an important part of our work.

2025-26 Dialogues and Engagement

This background is all important to how we approached engagement for the 2026 proxy season. We planned over the summer of 2025 with our partners at Rhia Ventures, a nonprofit that works to advance policies that protect reproductive and maternal health, and Whistlestop Capital, a consultancy that uses engagement strategies to encourage improved corporate practices.

As a reminder, many Clean Yield clients hold stocks in their portfolios that are not part of Clean Yield’s investment strategies, for a variety of reasons. We often engage with these companies when we feel that they have a particular exposure to an issue we are working on. This year, we also engaged with several companies held widely across our client portfolios, as we believe that our engagements on behalf of our clients can add value to these companies.

For the last few years, Clean Yield’s shareholder engagement has focused on equity and inclusion, as well as access to reproductive health care. We strongly believe that the companies that are viewed as the best for their employees will be able to attract and retain the best workforces and have a higher likelihood of financial success. Despite our clear belief that strong DEI programs at companies are a component of strong human capital management, we recognized that asking companies for EEO-1 data was not likely to result in meaningful dialogue this year.

Human Capital Management

Because of this, we pivoted a bit this year. Instead of asking for pure data disclosure, we engaged two companies on the topic of employee retention. Specifically, we asked Uber Technologies and Ferguson Enterprises to disclose employee retention rates by categories including veteran status, age, gender, race, and disability status. The conversation with plumbing distributor Ferguson was a bit simpler. That company has recently switched its domicile from the U.K. to the U.S. and had not previously faced a shareholder resolution. Ferguson quickly agreed to publish the data we requested, which is available on the company’s Sustainability page (data available as of June 2026). Learn more about Clean Yield’s analysis of Ferguson in our stock profile.

The conversation with Uber was more challenging. Through several rounds of dialogue, the company assured us that it is very data driven, and they do pay attention to the issues we raised—but were not willing to disclose the data we requested. The engagement culminated in a conversation with the Global Senior Director (employed according to LinkedIn as of June 2026) responsible for inclusion, which detailed many impressive programs and how the company uses data to ensure that its focus on culture complies with executive orders written to block consideration of DEI. While the company did not budge on disclosure, we did withdraw the resolution. We do feel that this type of engagement, where Investor Relations hears how important investors find issues such as inclusion, and hears from the in-house expert in more detail than they may have previously done so, can also raise the importance of the issues internally.

Our third human capital engagement took a different tactic. We approached Home Depot to ask them about the health insurance plans offered to employees. Specifically, given the concentration of employees in states with less access to quality health care, and the importance of store employees to the company’s success, we asked the company to describe how it determined if the health insurance plans offered to employees were sufficient in terms of access to timely, quality healthcare, because our research found that the out-of-pocket deductible could total more than 10% of many Home Depot employees’ take home pay. This was a novel approach for a proposal. Our discussion lasted several months, but we were unable to negotiate an agreement to withdraw our proposal. Due to the changes that were mentioned earlier, we were not able to communicate our rationale for this resolution on the SEC’s EDGAR database as in prior years, but we did provide information on our own website as well as those of several nonprofits that stepped up to fill the void, including As You Sow’s Proxy Open Exchange (POE). At the annual General Meeting in May, the proposal received 8% of the vote. We feel that for a novel proposal in this proxy voting environment, where the largest investors are reflexively voting with management, this vote total does indicate considerable investor interest, and we may pursue similar engagements in this upcoming year.

Reproductive and Maternal Health

Our engagements on reproductive and maternal health care have a similar underpinning. Lack of access to reproductive health care can both threaten employees’ health and well-being, as well as result in lower productivity or lost work time. In addition, jobs located in states with reproductive health care restrictions may not be attractive to top talent, all to the detriment of the employer. As an independent investment advisor, we have more freedom to engage companies on potentially controversial subjects than larger or non-independent firms, and reproductive health is firmly in this category. We approached three companies on the topic of employee access to reproductive health care in states with strict abortion laws.

As in prior years, one of the companies, in this case a basic materials manufacturer, requested confidentiality in order to have a candid discussion about the very solid benefits it provides to employees. On the other hand, we had a great discussion with Chipotle Mexican Grill about the company’s comprehensive benefits for its employees, which the company was eager to tell us about. Read our stock profile on Chipotle to review more of our analysis of the company.

Our conversation with a small-cap food producer, which also requested confidentiality, was more nuanced. While many larger companies self-fund their insurance programs and, therefore, have more input about the program’s design, this company is a smaller employer. This means the company is, to a certain extent, stuck with what its insurance provider will offer and more tied to state laws. We raised a variety of issues for the company to consider as it selects insurance providers in the future, and as it (hopefully!) grows in scale and switches to a self-insured model.

Proxy Voting

The final leg of our advocacy platform is proxy voting. Each year, we receive ballots for the annual general meetings of each company that any of our clients own. Like many other investors, we rely on specialist firms to help us analyze and process these ballots, in line with our voting guidelines. This year, several levels of government are taking aim at these proxy advisors, with bills introduced in 13 states and expectations at the federal level to limit investors’ abilities to use proxy advisors. This is one of the issues we spoke with Congressional staffers about at Hill Day in June.

Proxy Voting Guidelines

The proxy voting guidelines we use help instruct us on how to vote on issues at the meetings. The most common issue we vote on is the election of directors. We vote against — or withhold our votes from, in proxy parlance — directors for a variety of reasons, such as:

- Overboarding: Directors serving on more than 3 boards, or more than 2 boards if also a senior executive, can potentially compromise a director’s ability to fulfill their duties effectively in each role

- Attendance: Directors with attendance at less than 75% of meetings during the fiscal year

- Independence:

- Members of the nominating committee and the Chair if the Chair is not independent

- Members of the nominating committee and non-independent directors if less than 66% of directors are independent

- Members of the nominating, compensation or audit committees who are not independent

- Directors have been on the board for 9+ years

- Board diversity: Nominating committee members where the proposed slate

- Is not at least 40% gender diverse

- Is not at least 20% ethnically diverse

- The gender and/or ethnic composition of the board is not disclosed

In addition, we often vote against executive pay packages, which are up for vote at most companies at least every three years. The primary reason we vote against pay packages is based on the CEO pay ratio, specifically when the CEO’s compensation exceeds 100 times that of the company’s median employee.

On other topics, including shareholder proposals, our guidelines instruct us to vote in line with Clean Yield’s investment values.

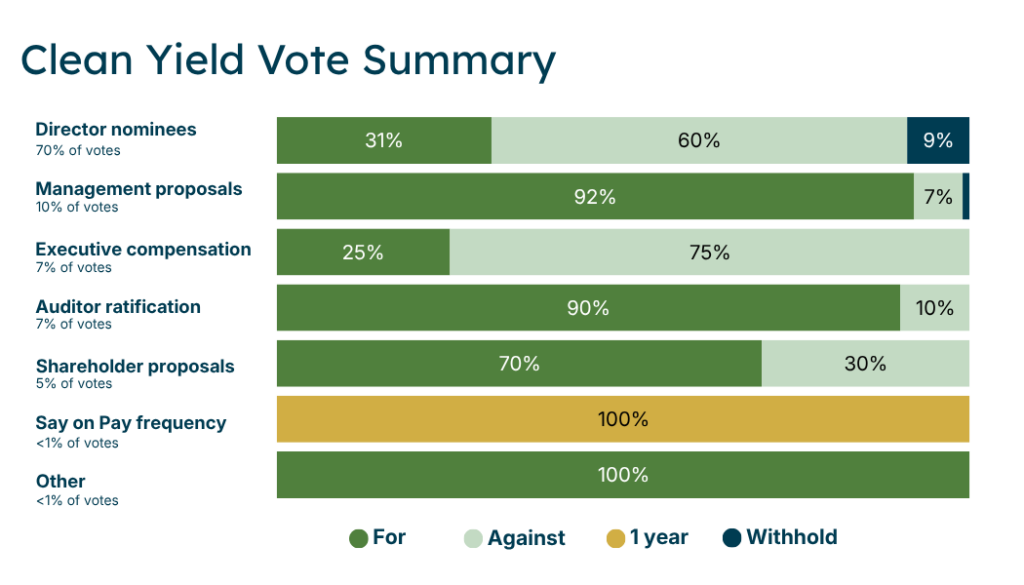

Votes Cast

Using these guidelines, we voted with management 40% of the time, for 31% of directors, and for 22% of executive compensation packages. We voted for 70% of shareholder proposals, some of which included topics such as:

- Water risk disclosure at Digital Realty Trust,

- Lobbying alignment at JPMorgan Chase,

- Reporting on ingredient-related risks at Coca-Cola,

- Reporting on AI use and oversight at Alphabet (Google), Meta Platforms (Facebook), Walmart, and Royal Bank of Canada,

- Human rights at Chevron, Intel and Microsoft, and

- Our own employee health care access resolution at Home Depot.

Chart data from Iconik.

Anti-DEI and Anti-ESG Resolutions

As discussed above, given the overall climate, it’s perhaps not surprising that the number of “anti-ESG” or “anti-DEI” shareholder proposals has continued to increase this year, despite their dismal showing last year, averaging 1-2%. We voted against 15 anti-DEI resolutions at companies this cycle, including at Home Depot and IBM on discrimination in charitable support (i.e. resolutions complaining that HD and IBM scores well on the Human Rights Campaign’s scorecard and therefore must be “promoting” transgender activism). Other shareholder proposals we voted against included:

- Evaluation of recycled plastics targets at Home Depot,

- Non-fiduciary (such as diversity or sustainability related) metrics used to evaluate executive compensation at Colgate-Palmolive, Gilead, Verizon and Allstate,

- Impacts of climate change commitments at Amazon and Next Era, and

- Report on coverage of transgender health care treatment for minors at American Express.

Summary

We believe that as equity investors who own a share of the companies we invest in, engaged ownership is part of our duty to seek financial, environmental and social performance from our companies. We are concerned about upcoming challenges we, and other investors, may face in carrying out this responsibility. But as we have noted previously, we believe that standing together with, and learning from, our community of like-minded investors working toward positive social and environmental change is more important now than ever. That’s why we find our membership in organizations such as US SIF, the Interfaith Center for Corporate Responsibility (ICCR), Ceres, and the Shareholder Rights Group so valuable. And it’s why we are committed to communicating to you about this work, through our newsletter, blog, and updates such as this.

To stay informed about shareholder advocacy updates, sign up for our newsletter.

Liz Levy is responsible for researching publicly traded equities and managing client portfolios, having joined Clean Yield in June 2024. She brings more than 20 years of experience in Sustainable Investing. She is a Chartered Financial Analyst and is passionate about aligning investment portfolios with values, with deep experience in managing divested, fossil fuel-free, and clean energy investments.

More News & Insights

Charitable Giving: How to Align Philanthropy and Donations with Your Financial Goals

Build Giving to Causes That Are Important to You into Your Financial Planning Philanthropy and charitable donations…

Q2 2026 Market Outlook: Investing in a Time of Dichotomies

A review of the market in Q2 and our plans for the market uncertainties in Q3.

Estate Planning for LGBTQIA+ Families: The Essential Documents to Have in Place

How to Protect Your Family and Your Assets For all families, estate planning is a critical process…